财经论丛 ›› 2022, Vol. 38 ›› Issue (3): 56-67.

吉利, 牟佳琪, 董雅浩

收稿日期:2021-05-10

出版日期:2022-03-10

发布日期:2022-03-10

作者简介:吉利(1978—),女,四川成都人,西南财经大学会计学院教授,博士生导师;基金资助:JI Li, MOU Jiaqi, DONG Yahao

Received:2021-05-10

Online:2022-03-10

Published:2022-03-10

摘要:

本文以我国重污染行业上市公司为样本,结合各地环境法规和规章及上市公司环保投入资本性支出和费用性支出等数据,进行实证研究发现:地方环境法规和规章数显著影响上市公司审计费用,二者正相关;上市公司前期“投资预防型”环保投入负向调节二者之间的正相关关系,表明“投资预防型”环保投入能够缓解环境规制对审计费用的影响,但“费损清偿型”环保投入不具备这种调节作用。本文创新性地划分并检验了异质性企业环保投入策略在缓解环境规制影响中的不同作用,揭示了环境规制影响审计费用以及企业环保投入可以作为一种风险管理工具的作用机制,对环境规制下审计行为的调整和企业环保行为的优化具有参考价值。

中图分类号:

吉利, 牟佳琪, 董雅浩. 环境规制、异质性企业环保投入策略与审计费用[J]. 财经论丛, 2022, 38(3): 56-67.

JI Li, MOU Jiaqi, DONG Yahao. Environmental Regulation, Heterogeneous Environmental Investment Strategies and Audit Fees[J]. Collected Essays on Finance and Economics, 2022, 38(3): 56-67.

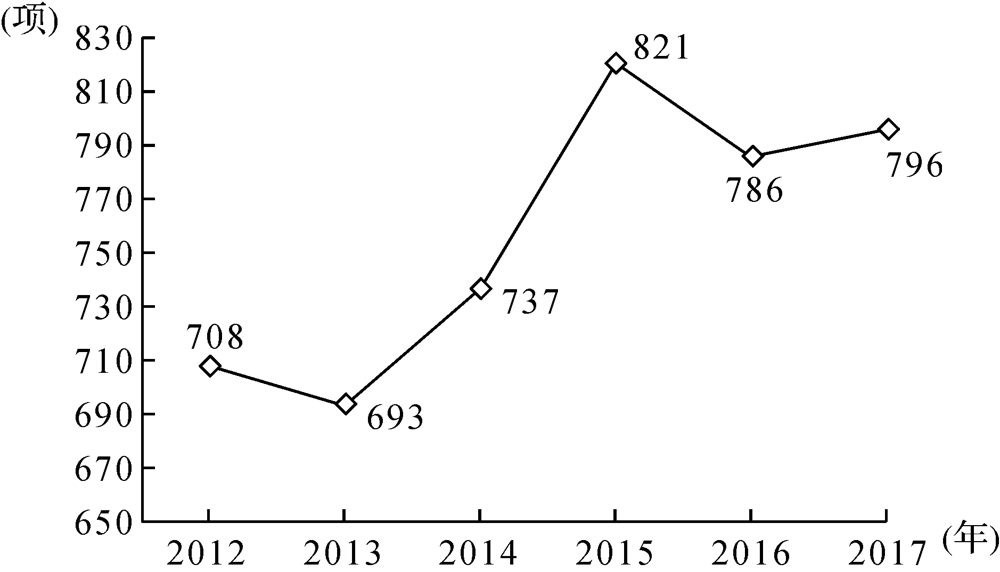

图1 2012—2017年现行有效地方环境法规和规章总数 数据来源:根据2012—2017年《中国环境年鉴》中相关数据统计所得。

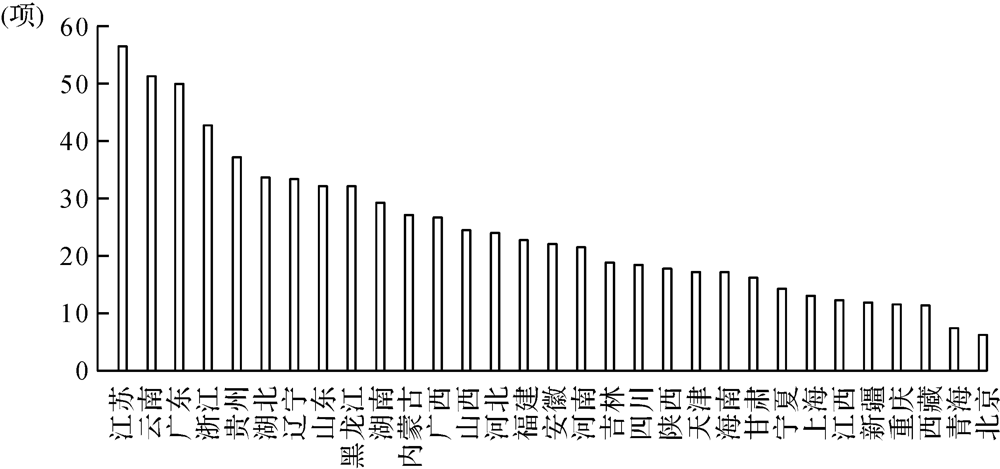

图2 2012—2017年各地现行有效地方环境法规和规章总数的年平均值 数据来源:根据2012—2017年《中国环境年鉴》中相关数据统计所得。

| 类型 | 名称 | 代码 | 定义 |

|---|---|---|---|

| 被解释变量 | 审计费用 | AuditFee | 公司当年审计费用/总资产* 10000 |

| 解释变量 | 环境法规和规章 | OnLALR | 公司注册地所在省现行有效地方环境法规和规章数之和 |

| 环境法规 | OnLA | 公司注册地所在省现行有效地方环境法规数 | |

| 环境规章 | OnLR | 公司注册地所在省现行有效地方环境规章数 | |

| 调节变量 | “投资预防型”环保投入 | Pinv_C | 公司“在建工程”附注中与环保有关项目的本期增加额的自然对数 |

| “费损清偿型”环保投入 | CostFee | 公司“管理费用”“营业外支出”和“营业税金及附加”附注中与环保有关项目的金额之和的自然对数 | |

| 控制变量 | 企业规模 | Size | 年末总资产的自然对数 |

| 资产收益率 | ROA | 资产收益率=净利润/总资产 | |

| 资产负债率 | Lev | 资产负债率=总负债/总资产 | |

| 企业价值 | TobinQ | 市值/资产总计 | |

| 业务复杂度 | AIRATIO | 应收账款净额与存货净额之和除以总资产 | |

| 股权集中度 | TOPONE | 第一大股东持股比例 | |

| 两职合一 | DUAL | 董事长与总经理兼任取值为1,否则为0 | |

| 独立董事比例 | IND | 独立董事人数/董事会人数 | |

| 是否“四大” | Audit4 | 会计师事务所为国际“四大”取值为1,否则为0 | |

| 审计意见类型 | Opinion | 若为标准无保留审计意见取值为1,否则为0 | |

| 行业 | Ind | 若观测值属于该行业则取值为1,否则为0 | |

| 年份 | Year | 若观测值属于该年度则取值为1,否则为0 |

表1 变量定义

| 类型 | 名称 | 代码 | 定义 |

|---|---|---|---|

| 被解释变量 | 审计费用 | AuditFee | 公司当年审计费用/总资产* 10000 |

| 解释变量 | 环境法规和规章 | OnLALR | 公司注册地所在省现行有效地方环境法规和规章数之和 |

| 环境法规 | OnLA | 公司注册地所在省现行有效地方环境法规数 | |

| 环境规章 | OnLR | 公司注册地所在省现行有效地方环境规章数 | |

| 调节变量 | “投资预防型”环保投入 | Pinv_C | 公司“在建工程”附注中与环保有关项目的本期增加额的自然对数 |

| “费损清偿型”环保投入 | CostFee | 公司“管理费用”“营业外支出”和“营业税金及附加”附注中与环保有关项目的金额之和的自然对数 | |

| 控制变量 | 企业规模 | Size | 年末总资产的自然对数 |

| 资产收益率 | ROA | 资产收益率=净利润/总资产 | |

| 资产负债率 | Lev | 资产负债率=总负债/总资产 | |

| 企业价值 | TobinQ | 市值/资产总计 | |

| 业务复杂度 | AIRATIO | 应收账款净额与存货净额之和除以总资产 | |

| 股权集中度 | TOPONE | 第一大股东持股比例 | |

| 两职合一 | DUAL | 董事长与总经理兼任取值为1,否则为0 | |

| 独立董事比例 | IND | 独立董事人数/董事会人数 | |

| 是否“四大” | Audit4 | 会计师事务所为国际“四大”取值为1,否则为0 | |

| 审计意见类型 | Opinion | 若为标准无保留审计意见取值为1,否则为0 | |

| 行业 | Ind | 若观测值属于该行业则取值为1,否则为0 | |

| 年份 | Year | 若观测值属于该年度则取值为1,否则为0 |

| 变量 | 样本量 | 平均值 | 标准差 | 最小值 | 中位数 | 最大值 |

|---|---|---|---|---|---|---|

| AuditFee | 5,314 | 3.0360 | 2.4510 | 0.2214 | 2.4139 | 13.8639 |

| OnLALR | 5,314 | 30.2264 | 19.2819 | 3.0000 | 28.0000 | 105.0000 |

| OnLA | 5,314 | 17.3931 | 11.2733 | 2.0000 | 16.0000 | 46.0000 |

| OnLR | 5,314 | 12.8224 | 10.1126 | 0.0000 | 10.0000 | 59.0000 |

| Pinv_C | 5,314 | 4.9448 | 7.6365 | 0.0000 | 0.0000 | 20.7426 |

| CostFee | 5,314 | 7.0430 | 7.2281 | 0.0000 | 0.0000 | 17.9766 |

表2 主要变量描述性统计

| 变量 | 样本量 | 平均值 | 标准差 | 最小值 | 中位数 | 最大值 |

|---|---|---|---|---|---|---|

| AuditFee | 5,314 | 3.0360 | 2.4510 | 0.2214 | 2.4139 | 13.8639 |

| OnLALR | 5,314 | 30.2264 | 19.2819 | 3.0000 | 28.0000 | 105.0000 |

| OnLA | 5,314 | 17.3931 | 11.2733 | 2.0000 | 16.0000 | 46.0000 |

| OnLR | 5,314 | 12.8224 | 10.1126 | 0.0000 | 10.0000 | 59.0000 |

| Pinv_C | 5,314 | 4.9448 | 7.6365 | 0.0000 | 0.0000 | 20.7426 |

| CostFee | 5,314 | 7.0430 | 7.2281 | 0.0000 | 0.0000 | 17.9766 |

| 分组变量 | 观测值 | 均值 | T检验 | 中位数 | Z检验 |

|---|---|---|---|---|---|

| OnLALR | <中位数(N=2630) | 2.8326 | 0.4027*** (6.01) | 2.2392 | 0.3551*** (7.53) |

| >=中位数(N=2684) | 3.2353 | 2.5943 | |||

| OnLA | <中位数(N=2604) | 2.8362 | 0.3919*** (5.85) | 2.2283 | 0.3597*** (7.27) |

| >=中位数(N=2710) | 3.2281 | 2.5880 | |||

| OnLR | <中位数(N=2403) | 2.8725 | 0.2985*** (4.43) | 2.2938 | 0.2311*** (5.52) |

| >=中位数(N=2911) | 3.1710 | 2.5249 |

表3 差异性检验

| 分组变量 | 观测值 | 均值 | T检验 | 中位数 | Z检验 |

|---|---|---|---|---|---|

| OnLALR | <中位数(N=2630) | 2.8326 | 0.4027*** (6.01) | 2.2392 | 0.3551*** (7.53) |

| >=中位数(N=2684) | 3.2353 | 2.5943 | |||

| OnLA | <中位数(N=2604) | 2.8362 | 0.3919*** (5.85) | 2.2283 | 0.3597*** (7.27) |

| >=中位数(N=2710) | 3.2281 | 2.5880 | |||

| OnLR | <中位数(N=2403) | 2.8725 | 0.2985*** (4.43) | 2.2938 | 0.2311*** (5.52) |

| >=中位数(N=2911) | 3.1710 | 2.5249 |

| 变量 | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| OnLALR | 0.0073*** | 0.0030*** | ||||

| (4.26) | (2.65) | |||||

| OnLA | 0.0141*** | 0.0059*** | ||||

| (4.78) | (2.98) | |||||

| OnLR | 0.0091*** | 0.0037* | ||||

| (2.82) | (1.74) | |||||

| Controls | No | Yes | No | Yes | No | Yes |

| Ind/Year | Yes | Yes | Yes | Yes | Yes | Yes |

| Obs | 5,314 | 5,314 | 5,314 | 5,314 | 5,314 | 5,314 |

| Adj_R2 | 0.1181 | 0.6140 | 0.1189 | 0.6141 | 0.1164 | 0.6137 |

表4 环境规制与审计费用回归结果

| 变量 | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| OnLALR | 0.0073*** | 0.0030*** | ||||

| (4.26) | (2.65) | |||||

| OnLA | 0.0141*** | 0.0059*** | ||||

| (4.78) | (2.98) | |||||

| OnLR | 0.0091*** | 0.0037* | ||||

| (2.82) | (1.74) | |||||

| Controls | No | Yes | No | Yes | No | Yes |

| Ind/Year | Yes | Yes | Yes | Yes | Yes | Yes |

| Obs | 5,314 | 5,314 | 5,314 | 5,314 | 5,314 | 5,314 |

| Adj_R2 | 0.1181 | 0.6140 | 0.1189 | 0.6141 | 0.1164 | 0.6137 |

| 变量 | “投资预防型”环保投入 | “费损清偿型”环保投入 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | ||||

| OnLALR | 0.0053*** | 0.0025* | |||||||

| (4.04) | (1.71) | ||||||||

| OnLA | 0.0111*** | 0.0067*** | |||||||

| (4.81) | (2.63) | ||||||||

| OnLR | 0.0059** | 0.0012 | |||||||

| (2.43) | (0.44) | ||||||||

| OnLALR*Pinv_C | -0.0006*** | ||||||||

| (-3.52) | |||||||||

| OnLA*Pinv_C | -0.0011*** | ||||||||

| (-4.37) | |||||||||

| OnLR*Pinv_C | -0.0007* | ||||||||

| (-1.91) | |||||||||

| OnLALR*CostFee | 0.0001 | ||||||||

| (0.65) | |||||||||

| OnLA*CostFee | -0.0002 | ||||||||

| (-0.55) | |||||||||

| OnLR*CostFee | 0.0006 | ||||||||

| (1.61) | |||||||||

| Pinv_C | 0.0163*** | 0.0185*** | 0.0074 | ||||||

| (2.85) | (3.45) | (1.40) | |||||||

| CostFee | -0.0015 | 0.0043 | -0.0049 | ||||||

| (-0.25) | (0.74) | (-0.90) | |||||||

| Controls/Ind/Year | Yes | Yes | Yes | Yes | Yes | Yes | |||

| Obs | 5,314 | 5,314 | 5,314 | 5,314 | 5,314 | 5,314 | |||

| Adj_R2 | 0.6148 | 0.6154 | 0.6138 | 0.6139 | 0.6140 | 0.6138 | |||

表5 异质性环保投入策略调节作用回归结果

| 变量 | “投资预防型”环保投入 | “费损清偿型”环保投入 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | ||||

| OnLALR | 0.0053*** | 0.0025* | |||||||

| (4.04) | (1.71) | ||||||||

| OnLA | 0.0111*** | 0.0067*** | |||||||

| (4.81) | (2.63) | ||||||||

| OnLR | 0.0059** | 0.0012 | |||||||

| (2.43) | (0.44) | ||||||||

| OnLALR*Pinv_C | -0.0006*** | ||||||||

| (-3.52) | |||||||||

| OnLA*Pinv_C | -0.0011*** | ||||||||

| (-4.37) | |||||||||

| OnLR*Pinv_C | -0.0007* | ||||||||

| (-1.91) | |||||||||

| OnLALR*CostFee | 0.0001 | ||||||||

| (0.65) | |||||||||

| OnLA*CostFee | -0.0002 | ||||||||

| (-0.55) | |||||||||

| OnLR*CostFee | 0.0006 | ||||||||

| (1.61) | |||||||||

| Pinv_C | 0.0163*** | 0.0185*** | 0.0074 | ||||||

| (2.85) | (3.45) | (1.40) | |||||||

| CostFee | -0.0015 | 0.0043 | -0.0049 | ||||||

| (-0.25) | (0.74) | (-0.90) | |||||||

| Controls/Ind/Year | Yes | Yes | Yes | Yes | Yes | Yes | |||

| Obs | 5,314 | 5,314 | 5,314 | 5,314 | 5,314 | 5,314 | |||

| Adj_R2 | 0.6148 | 0.6154 | 0.6138 | 0.6139 | 0.6140 | 0.6138 | |||

| 变量 | 央企 | 地方国企 | 非国有企业 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| OnLALR | -0.0016 | 0.0048* | 0.0065*** | ||||||

| (-0.43) | (1.80) | (3.96) | |||||||

| OnLA | -0.0095 | 0.0040 | 0.0164*** | ||||||

| (-1.43) | (0.83) | (5.77) | |||||||

| OnLR | 0.0047 | 0.0115** | 0.0040 | ||||||

| (0.66) | (2.44) | (1.32) | |||||||

| 变量 | 央企 | 地方国企 | 非国有企业 | ||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| OnLALR*Pinv_C | 0.0001 | -0.0006** | -0.0005* | ||||||

| (0.29) | (-2.32) | (-1.89) | |||||||

| OnLA*Pinv_C | 0.0005 | -0.0007 | -0.0012*** | ||||||

| (0.83) | (-1.50) | (-2.98) | |||||||

| OnLR*Pinv_C | -0.0000 | -0.0015*** | -0.0003 | ||||||

| (-0.06) | (-2.66) | (-0.57) | |||||||

| Pinv_C | -0.0018 | -0.0051 | 0.0011 | 0.0142* | 0.0076 | 0.0139* | 0.0184* | 0.0253*** | 0.0065 |

| (-0.18) | (-0.55) | (0.12) | (1.65) | (0.92) | (1.80) | (1.93) | (2.86) | (0.76) | |

| Controls/Ind/Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Obs | 658 | 658 | 658 | 1,436 | 1,436 | 1,436 | 3,220 | 3,220 | 3,220 |

| Adj_R2 | 0.6620 | 0.6630 | 0.6622 | 0.6154 | 0.6145 | 0.6161 | 0.6170 | 0.6191 | 0.6153 |

表6 企业产权性质分组回归结果

| 变量 | 央企 | 地方国企 | 非国有企业 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| OnLALR | -0.0016 | 0.0048* | 0.0065*** | ||||||

| (-0.43) | (1.80) | (3.96) | |||||||

| OnLA | -0.0095 | 0.0040 | 0.0164*** | ||||||

| (-1.43) | (0.83) | (5.77) | |||||||

| OnLR | 0.0047 | 0.0115** | 0.0040 | ||||||

| (0.66) | (2.44) | (1.32) | |||||||

| 变量 | 央企 | 地方国企 | 非国有企业 | ||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| OnLALR*Pinv_C | 0.0001 | -0.0006** | -0.0005* | ||||||

| (0.29) | (-2.32) | (-1.89) | |||||||

| OnLA*Pinv_C | 0.0005 | -0.0007 | -0.0012*** | ||||||

| (0.83) | (-1.50) | (-2.98) | |||||||

| OnLR*Pinv_C | -0.0000 | -0.0015*** | -0.0003 | ||||||

| (-0.06) | (-2.66) | (-0.57) | |||||||

| Pinv_C | -0.0018 | -0.0051 | 0.0011 | 0.0142* | 0.0076 | 0.0139* | 0.0184* | 0.0253*** | 0.0065 |

| (-0.18) | (-0.55) | (0.12) | (1.65) | (0.92) | (1.80) | (1.93) | (2.86) | (0.76) | |

| Controls/Ind/Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Obs | 658 | 658 | 658 | 1,436 | 1,436 | 1,436 | 3,220 | 3,220 | 3,220 |

| Adj_R2 | 0.6620 | 0.6630 | 0.6622 | 0.6154 | 0.6145 | 0.6161 | 0.6170 | 0.6191 | 0.6153 |

| 变量 | 信息透明度高 | 信息透明度低 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | ||||

| OnLALR | -0.0004 | 0.0057*** | |||||||

| (-0.21) | (2.68) | ||||||||

| OnLA | 0.0015 | 0.0106*** | |||||||

| (0.50) | (2.92) | ||||||||

| OnLR | -0.0032 | 0.0074* | |||||||

| (-0.91) | (1.82) | ||||||||

| OnLALR*Pinv_C | -0.0001 | -0.0006** | |||||||

| (-0.29) | (-2.52) | ||||||||

| OnLA*Pinv_C | -0.0003 | -0.0011*** | |||||||

| (-0.97) | (-2.68) | ||||||||

| OnLR*Pinv_C | 0.0002 | -0.0010* | |||||||

| (0.48) | (-1.74) | ||||||||

| Pinv_C | 0.0023 | 0.0059 | -0.0022 | 0.0203** | 0.0195** | 0.0132* | |||

| (0.31) | (0.87) | (-0.32) | (2.37) | (2.45) | (1.68) | ||||

| Controls/Ind/Year | Yes | Yes | Yes | Yes | Yes | Yes | |||

| Obs | 2,381 | 2,381 | 2,381 | 2,381 | 2,381 | 2,381 | |||

| Adj_R2 | 0.6226 | 0.6227 | 0.6227 | 0.6053 | 0.6055 | 0.6045 | |||

表7 信息透明度分组回归结果

| 变量 | 信息透明度高 | 信息透明度低 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | ||||

| OnLALR | -0.0004 | 0.0057*** | |||||||

| (-0.21) | (2.68) | ||||||||

| OnLA | 0.0015 | 0.0106*** | |||||||

| (0.50) | (2.92) | ||||||||

| OnLR | -0.0032 | 0.0074* | |||||||

| (-0.91) | (1.82) | ||||||||

| OnLALR*Pinv_C | -0.0001 | -0.0006** | |||||||

| (-0.29) | (-2.52) | ||||||||

| OnLA*Pinv_C | -0.0003 | -0.0011*** | |||||||

| (-0.97) | (-2.68) | ||||||||

| OnLR*Pinv_C | 0.0002 | -0.0010* | |||||||

| (0.48) | (-1.74) | ||||||||

| Pinv_C | 0.0023 | 0.0059 | -0.0022 | 0.0203** | 0.0195** | 0.0132* | |||

| (0.31) | (0.87) | (-0.32) | (2.37) | (2.45) | (1.68) | ||||

| Controls/Ind/Year | Yes | Yes | Yes | Yes | Yes | Yes | |||

| Obs | 2,381 | 2,381 | 2,381 | 2,381 | 2,381 | 2,381 | |||

| Adj_R2 | 0.6226 | 0.6227 | 0.6227 | 0.6053 | 0.6055 | 0.6045 | |||

| 变量 | 审计师任期长 | 审计师任期短 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | ||||

| OnLALR | 0.0014 | 0.0061*** | |||||||

| (0.61) | (3.84) | ||||||||

| OnLA | 0.0043 | 0.0122*** | |||||||

| (1.09) | (4.39) | ||||||||

| OnLR | -0.0003 | 0.0075** | |||||||

| (-0.06) | (2.53) | ||||||||

| OnLALR*Pinv_C | -0.0002 | -0.0007*** | |||||||

| (-0.92) | (-3.26) | ||||||||

| OnLA*Pinv_C | -0.0005 | -0.0013*** | |||||||

| (-1.27) | (-3.97) | ||||||||

| OnLR*Pinv_C | -0.0001 | -0.0009* | |||||||

| (-0.24) | (-1.94) | ||||||||

| Pinv_C | 0.0040 | 0.0058 | -0.0013 | 0.0210*** | 0.0231*** | 0.0114* | |||

| (0.45) | (0.71) | (-0.16) | (2.87) | (3.39) | (1.70) | ||||

| Controls/Ind/Year | Yes | Yes | Yes | Yes | Yes | Yes | |||

| Obs | 1,441 | 1,441 | 1,441 | 3,873 | 3,873 | 3,873 | |||

| Adj_R2 | 0.6217 | 0.6219 | 0.6215 | 0.6127 | 0.6133 | 0.6116 | |||

表8 审计师任期分组回归结果

| 变量 | 审计师任期长 | 审计师任期短 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | ||||

| OnLALR | 0.0014 | 0.0061*** | |||||||

| (0.61) | (3.84) | ||||||||

| OnLA | 0.0043 | 0.0122*** | |||||||

| (1.09) | (4.39) | ||||||||

| OnLR | -0.0003 | 0.0075** | |||||||

| (-0.06) | (2.53) | ||||||||

| OnLALR*Pinv_C | -0.0002 | -0.0007*** | |||||||

| (-0.92) | (-3.26) | ||||||||

| OnLA*Pinv_C | -0.0005 | -0.0013*** | |||||||

| (-1.27) | (-3.97) | ||||||||

| OnLR*Pinv_C | -0.0001 | -0.0009* | |||||||

| (-0.24) | (-1.94) | ||||||||

| Pinv_C | 0.0040 | 0.0058 | -0.0013 | 0.0210*** | 0.0231*** | 0.0114* | |||

| (0.45) | (0.71) | (-0.16) | (2.87) | (3.39) | (1.70) | ||||

| Controls/Ind/Year | Yes | Yes | Yes | Yes | Yes | Yes | |||

| Obs | 1,441 | 1,441 | 1,441 | 3,873 | 3,873 | 3,873 | |||

| Adj_R2 | 0.6217 | 0.6219 | 0.6215 | 0.6127 | 0.6133 | 0.6116 | |||

| [1] | 李培功, 陈秀婷, 汶海. 社会规范、企业环境影响与审计收费惩戒——来自我国上市公司的经验证据[J]. 审计研究, 2018, (4):95-102. |

| [2] | 余海宗, 何娜, 夏常源. 地方政府环境规制与审计费用——来自民营重污染上市公司的经验证据[J]. 审计研究, 2018, (4):77-85. |

| [3] | 张红凤, 周峰, 杨慧, 等. 环境保护与经济发展双赢的规制绩效实证分析[J]. 经济研究, 2009, (3):14-26. |

| [4] | 李钢, 马岩, 姚磊磊. 中国工业环境管制强度与提升路线——基于中国工业环境保护成本与效益的实证研究[J]. 中国工业经济, 2010, (3):31-41. |

| [5] |

Murty M. N., Kumar S., Paul M. Environmental Regulation, Productive Efficiency and Cost of Pollution Abatement: A Case Study of the Sugar Industry in India[J]. Journal of Environmental Management, 2006, 79(1):1-9.

PMID |

| [6] | Joshi S., Krishnan R., Lave L. Estimating the Hidden Costs of Environmental Regulation[J]. Accounting Review, 2001. |

| [7] | 唐国平, 李龙会, 吴德军. 环境管制、行业属性与企业环保投资[J]. 会计研究, 2013, (6):83-89. |

| [8] | 景维民, 张璐. 环境管制、对外开放与中国工业的绿色技术进步[J]. 经济研究, 2014, (9):34-47. |

| [9] | 王锋正, 陈方圆. 董事会治理、环境规制与绿色技术创新——基于我国重污染行业上市公司的实证检验[J]. 科学学研究, 2018, (2):361-369. |

| [10] | 王超, 李真真, 蒋萍. 环境规制政策对中国重污染工业行业技术创新的影响机制研究[J]. 科研管理, 2021, (2):88-99. |

| [11] | 刘斌, 叶建中, 廖莹毅. 我国上市公司审计收费影响因素的实证研究——深沪市2001年报的经验证据[J]. 审计研究, 2003, (1):44-47. |

| [12] | 伍利娜. 审计定价影响因素研究——来自中国上市公司首次审计费用披露的证据[J]. 中国会计评论, 2003: 16. |

| [13] | 李嘉明, 杨帆. 对外担保会影响审计费用与审计意见吗?[J]. 审计与经济研究, 2016, (1):27-37. |

| [14] | 翟胜宝, 许浩然, 刘耀淞, 等. 控股股东股权质押与审计师风险应对[J]. 管理世界, 2017, (10):51-65. |

| [15] | 林晚发, 敖小波. 企业信用评级与审计收费[J]. 审计研究, 2018, (3):95-103. |

| [16] | 米莉, 黄婧, 何丽娜. 证券交易所非处罚性监管会影响审计师定价决策吗?——基于问询函的经验证据[J]. 审计与经济研究, 2019, (4):57-65. |

| [17] |

Godfrey P. C. The Relationship Between Corporate Philanthropy and Shareholder Wealth: A Risk Management Perspective[J]. Academy of Management Review, 2005, 30(4):777-798.

DOI URL |

| [18] | Shiu Y, Yang S. Does Engagement in Corporate Social Responsibility Provide Strategic Insurance-like Effects?[J]. Strategic Management Journal, 2017, 38(2). |

| [19] | 薛求知, 伊晟. 企业环保投入影响因素分析——从外部制度到内部资源和激励[J]. 软科学, 2015, (3):1-4, 51. |

| [20] | 王云, 李延喜, 马壮, 等. 媒体关注、环境规制与企业环保投资[J]. 南开管理评论, 2017, (6):83-94. |

| [21] | 张三峰, 卜茂亮. 环境规制、环保投入与中国企业生产率——基于中国企业问卷数据的实证研[J]. 南开经济研究, 2011, (2):129-146. |

| [22] | 姜英兵, 崔广慧. 环保产业政策对企业环保投资的影响: 基于重污染上市公司的经验证据[J]. 改革, 2019, (2):87-101. |

| [23] | 吉利, 苏朦. 企业环境成本内部化动因: 合规还是利益?——来自重污染行业上市公司的经验证据[J]. 会计研究, 2016, (11):69-75, 96. |

| [24] | 吉利, 苏朦. 中国上市公司环境成本内部化行为识别及特征剖析——基于财务报表信息的分析[J]. 河北经贸大学学报, 2017, (5):99-109. |

| [25] | 王建明. 环境信息披露、行业差异和外部制度压力相关性研究——来自我国沪市上市公司环境信息披露的经验证据[J]. 会计研究, 2008, (6):54-62, 95. |

| [26] | 李树, 翁卫国. 我国地方环境管制与全要素生产率增长——基于地方立法和行政规章实际效率的实证分析[J]. 财经研究, 2014, (2):19-29. |

| [27] | 王书斌, 徐盈之. 环境规制与雾霾脱钩效应——基于企业投资偏好的视角[J]. 中国工业经济, 2015, (4):18-30. |

| [28] | 朱松, 夏冬林, 陈长春. 审计任期与会计稳健性[J]. 审计研究, 2010, (3):89-95. |

| [29] | 陈小林, 张雪华, 闫焕民. 事务所转制、审计师个人特征与会计稳健性[J]. 会计研究, 2016, (6):77-85, 95. |

| [1] | 项后军, 张翔, 王利沙. 政府引导基金对企业风险承担的影响研究[J]. 财经论丛, 2024, 40(3): 16-25. |

| [2] | 盛皓炜, 王如忠. 数字经济对工业生态效率的影响——基于长三角城市群的实证分析[J]. 财经论丛, 2023, 39(9): 3-13. |

| [3] | 刘亦文, 周韶成. 正式与非正式环境规制政策协同的减污降碳效应研究[J]. 财经论丛, 2023, 39(8): 103-112. |

| [4] | 邵慰, 金泽斌, 陈子琦. 环境规制对区域生态效率的空间效应研究: 基于财政分权的调节作用[J]. 财经论丛, 2023, 39(6): 103-112. |

| [5] | 蔡海静, 王雪青, 谢乔昕. 环境规制视阈下文明城市评选对企业绿色创新的影响研究[J]. 财经论丛, 2023, 39(5): 102-112. |

| [6] | 李芳, 于寅健, 王松. 中小股东网络表达会影响审计师风险应对行为吗?——基于公司盈余管理的中介效应检验[J]. 财经论丛, 2023, 39(4): 69-79. |

| [7] | 周小亮, 林栋. 有限资本市场参与、收入分配与最优货币政策[J]. 财经论丛, 2023, 39(3): 15-24. |

| [8] | 许钊, 高煜, 霍治方. 智慧城市建设与数字普惠金融发展:作用机制与经验证据[J]. 财经论丛, 2023, 39(3): 47-56. |

| [9] | 郭丽娟, 沈沛龙. 银行异质性、系统性风险与宏观经济运行——兼论货币政策与宏观审慎政策的协调与搭配[J]. 财经论丛, 2023, 39(12): 58-69. |

| [10] | 唐国平, 孙洪锋, 陈曦. 碳排放权交易制度与企业投资行为[J]. 财经论丛, 2022, 38(4): 57-68. |

| [11] | 舒长江, 洪攀. 美联储货币政策不确定性对我国企业杠杆率的溢出效应——基于融资约束异质性视角[J]. 财经论丛, 2022, 38(12): 48-58. |

| [12] | 田淑英, 夏梦丽, 许文立. 低碳经济下的企业绩效及其信贷约束——基于“低碳城市”试点政策的准自然实验分析[J]. 财经论丛, 2022, 38(10): 49-58. |

| [13] | 鲁建坤, 纪珈雯, 丁明. 企业纳税贡献与环境治理投资[J]. 财经论丛, 2021, 37(9): 28-36. |

| [14] | 闫永生, 邵传林, 刘慧侠. 营商环境与民营企业创新——基于行政审批中心设立的准自然实验[J]. 财经论丛, 2021, 37(9): 93-103. |

| [15] | 胡小丽. 农村人口转移对城乡收入差距的影响——基于中国313个地级市的经验证据[J]. 财经论丛, 2021, 37(8): 3-13. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||