财经论丛 ›› 2021, Vol. 37 ›› Issue (9): 49-59.

赵飞

收稿日期:2021-01-07

出版日期:2021-09-10

发布日期:2021-09-16

作者简介:赵飞(1993-),男,河南新乡人,中南财经政法大学金融学院博士生。

基金资助:ZHAO Fei

Received:2021-01-07

Online:2021-09-10

Published:2021-09-16

摘要:

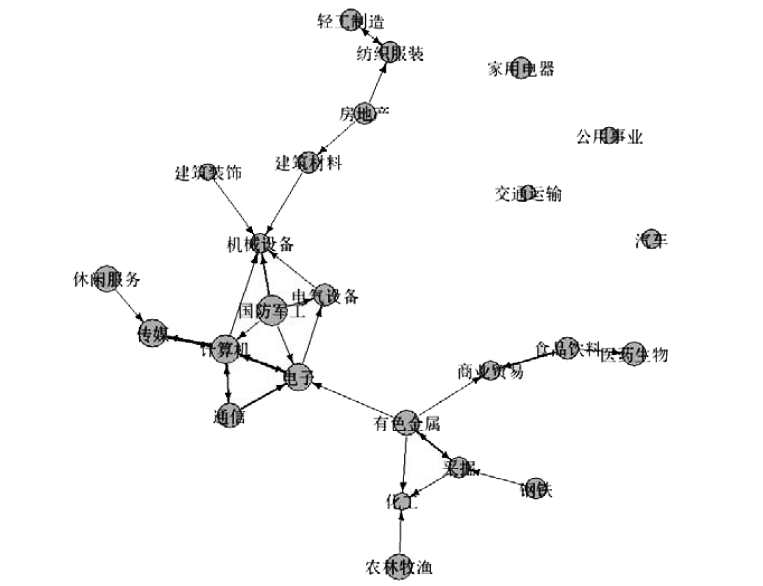

利用LASSO-CoVaR模型对我国实体行业风险溢出机制与特征进行分析,并利用行业特征数据考察实体行业风险溢出的影响因素。研究发现:我国实体行业尾部风险溢出总体水平呈现“近危机”特征,且不同行业的风险波动具有显著差异;以电子、计算机为代表的电子信息产业已经成为主要的风险溢出者,计算机、有色金属与国防军工为主要的风险吸收者;业务相关性较高的行业间尾部风险关联呈现出稳定的同质特征;行业自身风险和杠杆率等特征对行业尾部风险关联具有显著影响。

中图分类号:

赵飞. 实体行业风险溢出机制与特征分析[J]. 财经论丛, 2021, 37(9): 49-59.

ZHAO Fei. Analysis of Risk Spillover Mechanism and Characteristics among Real Industry[J]. Collected Essays on Finance and Economics, 2021, 37(9): 49-59.

图1 实体行业尾部风险溢出总体水平动态变化

| 行业 | 风险溢出 | 风险吸收 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 均值 | 中值 | 最小值 | 最大值 | 均值 | 中值 | 最小值 | 最大值 | |||||

| 采掘 | 0.07 | 0.07 | 0.02 | 0.18 | 0.11 | 0.09 | 0.01 | 0.38 | ||||

| 化工 | 0.15 | 0.13 | 0.03 | 0.82 | 0.08 | 0.07 | 0.04 | 0.26 | ||||

| 钢铁 | 0.06 | 0.06 | 0.01 | 0.20 | 0.11 | 0.10 | 0.03 | 0.34 | ||||

| 有色金属 | 0.09 | 0.08 | 0.02 | 0.27 | 0.14 | 0.13 | 0.03 | 0.33 | ||||

| 建筑材料 | 0.11 | 0.09 | 0.01 | 0.36 | 0.11 | 0.10 | 0.03 | 0.28 | ||||

| 建筑装饰 | 0.07 | 0.07 | 0 | 0.29 | 0.09 | 0.07 | 0.02 | 0.42 | ||||

| 电气设备 | 0.14 | 0.12 | 0.03 | 0.48 | 0.10 | 0.09 | 0.04 | 0.29 | ||||

| 机械设备 | 0.17 | 0.16 | 0.04 | 0.42 | 0.09 | 0.08 | 0.04 | 0.26 | ||||

| 国防军工 | 0.07 | 0.06 | 0.01 | 0.24 | 0.14 | 0.12 | 0.04 | 0.71 | ||||

| 汽车 | 0.09 | 0.07 | 0.02 | 0.41 | 0.10 | 0.08 | 0.02 | 0.24 | ||||

| 家用电器 | 0.07 | 0.06 | 0.02 | 0.25 | 0.11 | 0.11 | 0.02 | 0.31 | ||||

| 纺织服装 | 0.15 | 0.13 | 0.02 | 0.40 | 0.10 | 0.09 | 0.03 | 0.26 | ||||

| 轻工制造 | 0.17 | 0.15 | 0.04 | 0.46 | 0.10 | 0.08 | 0.04 | 0.23 | ||||

| 商业贸易 | 0.14 | 0.12 | 0.03 | 0.43 | 0.10 | 0.09 | 0.04 | 0.27 | ||||

| 农林牧渔 | 0.09 | 0.08 | 0.03 | 0.34 | 0.12 | 0.12 | 0.03 | 0.37 | ||||

| 食品饮料 | 0.08 | 0.07 | 0.01 | 0.22 | 0.12 | 0.11 | 0.02 | 0.31 | ||||

| 休闲服务 | 0.10 | 0.10 | 0.01 | 0.29 | 0.12 | 0.11 | 0.03 | 0.40 | ||||

| 医药生物 | 0.10 | 0.09 | 0.03 | 0.44 | 0.10 | 0.09 | 0.03 | 0.23 | ||||

| 公用事业 | 0.08 | 0.06 | 0.01 | 0.27 | 0.08 | 0.07 | 0.02 | 0.29 | ||||

| 交通运输 | 0.07 | 0.06 | 0.01 | 0.25 | 0.07 | 0.06 | 0.02 | 0.34 | ||||

| 房地产 | 0.06 | 0.06 | 0.01 | 0.17 | 0.11 | 0.11 | 0.02 | 0.41 | ||||

| 电子 | 0.19 | 0.18 | 0.04 | 0.62 | 0.12 | 0.11 | 0.04 | 0.23 | ||||

| 计算机 | 0.18 | 0.16 | 0.04 | 0.45 | 0.14 | 0.13 | 0.05 | 0.36 | ||||

| 传媒 | 0.12 | 0.10 | 0.02 | 0.59 | 0.13 | 0.12 | 0.04 | 0.34 | ||||

| 通信 | 0.08 | 0.07 | 0.01 | 0.28 | 0.11 | 0.10 | 0.04 | 0.44 | ||||

表1 我国各实体行业尾部风险关联基本统计量

| 行业 | 风险溢出 | 风险吸收 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 均值 | 中值 | 最小值 | 最大值 | 均值 | 中值 | 最小值 | 最大值 | |||||

| 采掘 | 0.07 | 0.07 | 0.02 | 0.18 | 0.11 | 0.09 | 0.01 | 0.38 | ||||

| 化工 | 0.15 | 0.13 | 0.03 | 0.82 | 0.08 | 0.07 | 0.04 | 0.26 | ||||

| 钢铁 | 0.06 | 0.06 | 0.01 | 0.20 | 0.11 | 0.10 | 0.03 | 0.34 | ||||

| 有色金属 | 0.09 | 0.08 | 0.02 | 0.27 | 0.14 | 0.13 | 0.03 | 0.33 | ||||

| 建筑材料 | 0.11 | 0.09 | 0.01 | 0.36 | 0.11 | 0.10 | 0.03 | 0.28 | ||||

| 建筑装饰 | 0.07 | 0.07 | 0 | 0.29 | 0.09 | 0.07 | 0.02 | 0.42 | ||||

| 电气设备 | 0.14 | 0.12 | 0.03 | 0.48 | 0.10 | 0.09 | 0.04 | 0.29 | ||||

| 机械设备 | 0.17 | 0.16 | 0.04 | 0.42 | 0.09 | 0.08 | 0.04 | 0.26 | ||||

| 国防军工 | 0.07 | 0.06 | 0.01 | 0.24 | 0.14 | 0.12 | 0.04 | 0.71 | ||||

| 汽车 | 0.09 | 0.07 | 0.02 | 0.41 | 0.10 | 0.08 | 0.02 | 0.24 | ||||

| 家用电器 | 0.07 | 0.06 | 0.02 | 0.25 | 0.11 | 0.11 | 0.02 | 0.31 | ||||

| 纺织服装 | 0.15 | 0.13 | 0.02 | 0.40 | 0.10 | 0.09 | 0.03 | 0.26 | ||||

| 轻工制造 | 0.17 | 0.15 | 0.04 | 0.46 | 0.10 | 0.08 | 0.04 | 0.23 | ||||

| 商业贸易 | 0.14 | 0.12 | 0.03 | 0.43 | 0.10 | 0.09 | 0.04 | 0.27 | ||||

| 农林牧渔 | 0.09 | 0.08 | 0.03 | 0.34 | 0.12 | 0.12 | 0.03 | 0.37 | ||||

| 食品饮料 | 0.08 | 0.07 | 0.01 | 0.22 | 0.12 | 0.11 | 0.02 | 0.31 | ||||

| 休闲服务 | 0.10 | 0.10 | 0.01 | 0.29 | 0.12 | 0.11 | 0.03 | 0.40 | ||||

| 医药生物 | 0.10 | 0.09 | 0.03 | 0.44 | 0.10 | 0.09 | 0.03 | 0.23 | ||||

| 公用事业 | 0.08 | 0.06 | 0.01 | 0.27 | 0.08 | 0.07 | 0.02 | 0.29 | ||||

| 交通运输 | 0.07 | 0.06 | 0.01 | 0.25 | 0.07 | 0.06 | 0.02 | 0.34 | ||||

| 房地产 | 0.06 | 0.06 | 0.01 | 0.17 | 0.11 | 0.11 | 0.02 | 0.41 | ||||

| 电子 | 0.19 | 0.18 | 0.04 | 0.62 | 0.12 | 0.11 | 0.04 | 0.23 | ||||

| 计算机 | 0.18 | 0.16 | 0.04 | 0.45 | 0.14 | 0.13 | 0.05 | 0.36 | ||||

| 传媒 | 0.12 | 0.10 | 0.02 | 0.59 | 0.13 | 0.12 | 0.04 | 0.34 | ||||

| 通信 | 0.08 | 0.07 | 0.01 | 0.28 | 0.11 | 0.10 | 0.04 | 0.44 | ||||

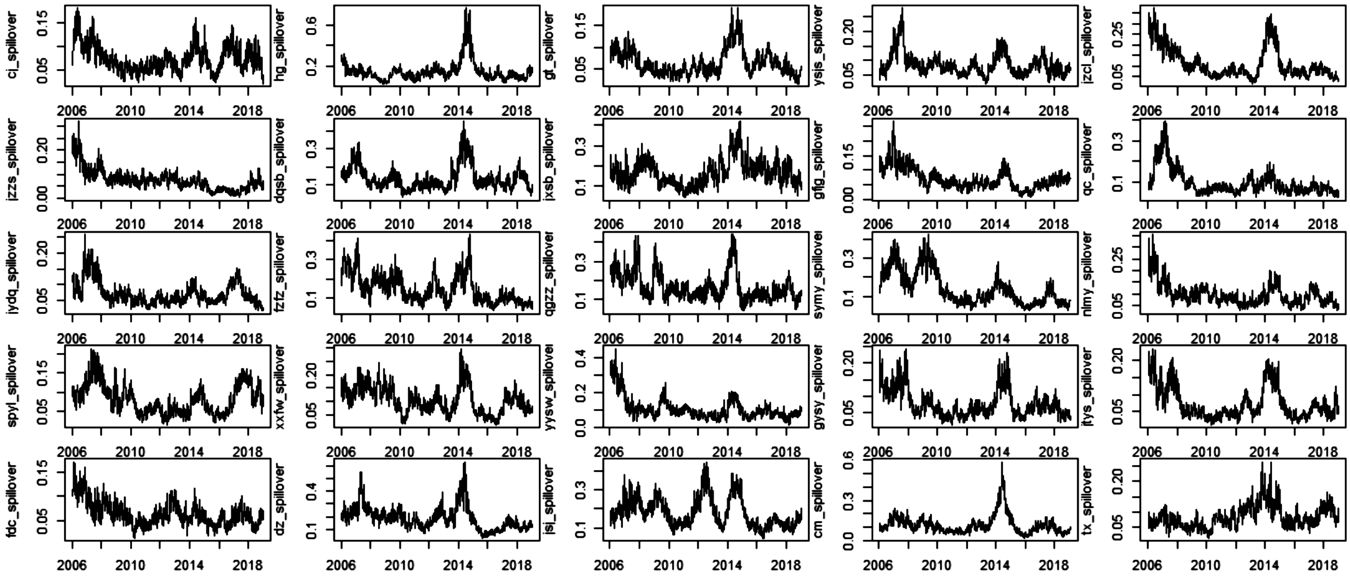

图2 我国各实体行业风险溢出水平动态变化

图3 我国各实体行业风险吸收水平动态变化

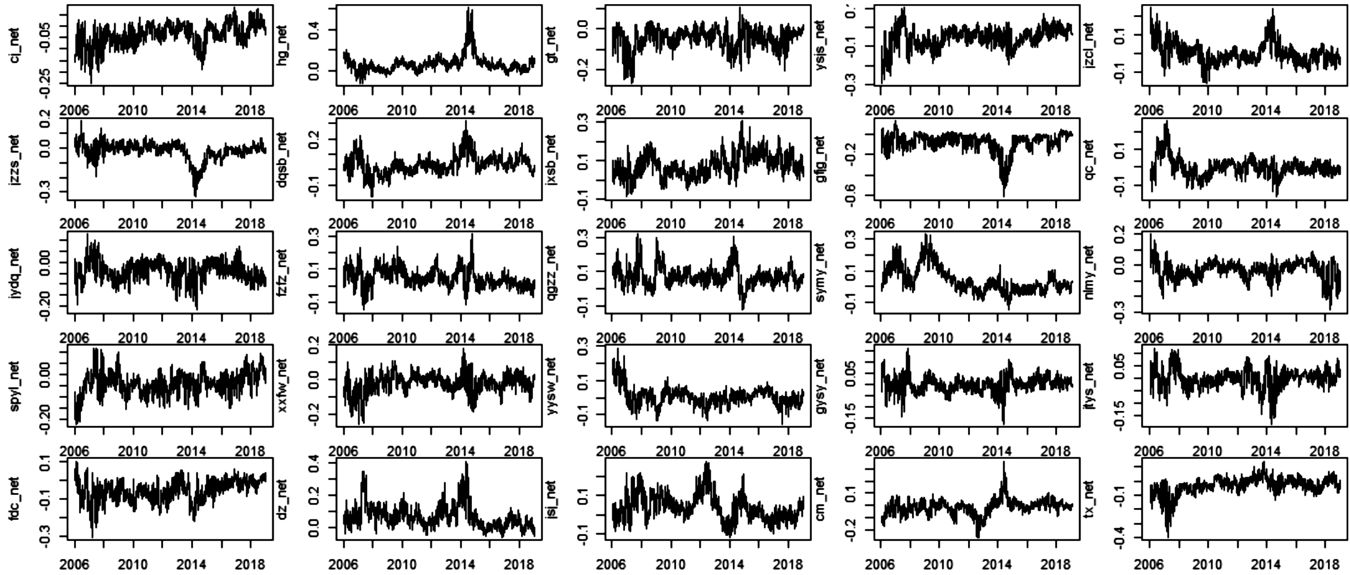

图4 我国各实体行业净风险效应动态变化

图5 全样本下实体行业尾部风险关联网络

| 行业 | 风险溢出 | 风险吸收 | 净风险效应 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 危机时期 | 正常时期 | 危机时期 | 正常时期 | 危机时期 | 正常时期 | ||||||

| 采掘 | 0.09 | 0.06 | 0.16 | 0.09 | -0.07 | -0.02 | |||||

| 化工 | 0.22 | 0.11 | 0.11 | 0.07 | 0.10 | 0.05 | |||||

| 钢铁 | 0.09 | 0.05 | 0.16 | 0.09 | -0.07 | -0.04 | |||||

| 有色金属 | 0.11 | 0.07 | 0.18 | 0.12 | -0.07 | -0.04 | |||||

| 建筑材料 | 0.19 | 0.07 | 0.14 | 0.09 | 0.05 | -0.02 | |||||

| 建筑装饰 | 0.10 | 0.06 | 0.15 | 0.07 | -0.05 | 0 | |||||

| 电气设备 | 0.19 | 0.11 | 0.14 | 0.08 | 0.06 | 0.02 | |||||

| 机械设备 | 0.20 | 0.15 | 0.13 | 0.07 | 0.07 | 0.08 | |||||

| 国防军工 | 0.10 | 0.06 | 0.23 | 0.10 | -0.13 | -0.05 | |||||

| 汽车 | 0.15 | 0.07 | 0.13 | 0.08 | 0.01 | -0.01 | |||||

| 家用电器 | 0.09 | 0.06 | 0.13 | 0.10 | -0.03 | -0.04 | |||||

| 纺织服装 | 0.20 | 0.12 | 0.14 | 0.08 | 0.06 | 0.04 | |||||

| 行业 | 风险溢出 | 风险吸收 | 净风险效应 | ||||||||

| 危机时期 | 正常时期 | 危机时期 | 正常时期 | 危机时期 | 正常时期 | ||||||

| 轻工制造 | 0.22 | 0.14 | 0.13 | 0.08 | 0.08 | 0.07 | |||||

| 商业贸易 | 0.19 | 0.12 | 0.14 | 0.08 | 0.04 | 0.04 | |||||

| 农林牧渔 | 0.13 | 0.08 | 0.16 | 0.11 | -0.03 | -0.03 | |||||

| 食品饮料 | 0.10 | 0.07 | 0.14 | 0.11 | -0.04 | -0.03 | |||||

| 休闲服务 | 0.14 | 0.09 | 0.18 | 0.09 | -0.04 | -0.01 | |||||

| 医药生物 | 0.14 | 0.09 | 0.12 | 0.09 | 0.02 | 0 | |||||

| 公用事业 | 0.12 | 0.06 | 0.12 | 0.06 | 0 | 0 | |||||

| 交通运输 | 0.12 | 0.05 | 0.13 | 0.05 | 0 | 0 | |||||

| 房地产 | 0.08 | 0.06 | 0.15 | 0.10 | -0.07 | -0.04 | |||||

| 电子 | 0.27 | 0.15 | 0.15 | 0.11 | 0.12 | 0.05 | |||||

| 计算机 | 0.21 | 0.16 | 0.18 | 0.12 | 0.03 | 0.04 | |||||

| 传媒 | 0.17 | 0.09 | 0.17 | 0.11 | 0 | -0.02 | |||||

| 通信 | 0.10 | 0.07 | 0.16 | 0.09 | -0.06 | -0.02 | |||||

表2 不同风险状态下实体行业尾部风险网络角色分析

| 行业 | 风险溢出 | 风险吸收 | 净风险效应 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 危机时期 | 正常时期 | 危机时期 | 正常时期 | 危机时期 | 正常时期 | ||||||

| 采掘 | 0.09 | 0.06 | 0.16 | 0.09 | -0.07 | -0.02 | |||||

| 化工 | 0.22 | 0.11 | 0.11 | 0.07 | 0.10 | 0.05 | |||||

| 钢铁 | 0.09 | 0.05 | 0.16 | 0.09 | -0.07 | -0.04 | |||||

| 有色金属 | 0.11 | 0.07 | 0.18 | 0.12 | -0.07 | -0.04 | |||||

| 建筑材料 | 0.19 | 0.07 | 0.14 | 0.09 | 0.05 | -0.02 | |||||

| 建筑装饰 | 0.10 | 0.06 | 0.15 | 0.07 | -0.05 | 0 | |||||

| 电气设备 | 0.19 | 0.11 | 0.14 | 0.08 | 0.06 | 0.02 | |||||

| 机械设备 | 0.20 | 0.15 | 0.13 | 0.07 | 0.07 | 0.08 | |||||

| 国防军工 | 0.10 | 0.06 | 0.23 | 0.10 | -0.13 | -0.05 | |||||

| 汽车 | 0.15 | 0.07 | 0.13 | 0.08 | 0.01 | -0.01 | |||||

| 家用电器 | 0.09 | 0.06 | 0.13 | 0.10 | -0.03 | -0.04 | |||||

| 纺织服装 | 0.20 | 0.12 | 0.14 | 0.08 | 0.06 | 0.04 | |||||

| 行业 | 风险溢出 | 风险吸收 | 净风险效应 | ||||||||

| 危机时期 | 正常时期 | 危机时期 | 正常时期 | 危机时期 | 正常时期 | ||||||

| 轻工制造 | 0.22 | 0.14 | 0.13 | 0.08 | 0.08 | 0.07 | |||||

| 商业贸易 | 0.19 | 0.12 | 0.14 | 0.08 | 0.04 | 0.04 | |||||

| 农林牧渔 | 0.13 | 0.08 | 0.16 | 0.11 | -0.03 | -0.03 | |||||

| 食品饮料 | 0.10 | 0.07 | 0.14 | 0.11 | -0.04 | -0.03 | |||||

| 休闲服务 | 0.14 | 0.09 | 0.18 | 0.09 | -0.04 | -0.01 | |||||

| 医药生物 | 0.14 | 0.09 | 0.12 | 0.09 | 0.02 | 0 | |||||

| 公用事业 | 0.12 | 0.06 | 0.12 | 0.06 | 0 | 0 | |||||

| 交通运输 | 0.12 | 0.05 | 0.13 | 0.05 | 0 | 0 | |||||

| 房地产 | 0.08 | 0.06 | 0.15 | 0.10 | -0.07 | -0.04 | |||||

| 电子 | 0.27 | 0.15 | 0.15 | 0.11 | 0.12 | 0.05 | |||||

| 计算机 | 0.21 | 0.16 | 0.18 | 0.12 | 0.03 | 0.04 | |||||

| 传媒 | 0.17 | 0.09 | 0.17 | 0.11 | 0 | -0.02 | |||||

| 通信 | 0.10 | 0.07 | 0.16 | 0.09 | -0.06 | -0.02 | |||||

| 风险溢出行业 | 风险吸收 行业 | 危机时期 强度排名 | 正常时期 强度排名 | 排名 变动 | 风险溢出行业 | 风险吸收 行业 | 危机时期 强度排名 | 正常时期 强度排名 | 排名 变动 |

|---|---|---|---|---|---|---|---|---|---|

| 稳定关联: | 非稳定关联: | ||||||||

| 通信 | 计算机 | 4 | 5 | 1 | 国防军工 | 传媒 | 66 | 598 | 532 |

| 计算机 | 电子 | 1 | 2 | 1 | 交通运输 | 机械设备 | 74 | 551 | 477 |

| 传媒 | 计算机 | 2 | 1 | 1 | 电气设备 | 建筑材料 | 143 | 587 | 444 |

| 国防军工 | 机械设备 | 12 | 10 | 2 | 国防军工 | 建筑材料 | 44 | 476 | 432 |

| 钢铁 | 采掘 | 37 | 34 | 3 | 建筑材料 | 传媒 | 109 | 525 | 416 |

| 采掘 | 有色金属 | 5 | 8 | 3 | 传媒 | 食品饮料 | 181 | 563 | 382 |

| 国防军工 | 电气设备 | 10 | 31 | 21 | 国防军工 | 轻工制造 | 574 | 203 | 371 |

表3 不同风险状态下实体行业间风险传染排名变化分析

| 风险溢出行业 | 风险吸收 行业 | 危机时期 强度排名 | 正常时期 强度排名 | 排名 变动 | 风险溢出行业 | 风险吸收 行业 | 危机时期 强度排名 | 正常时期 强度排名 | 排名 变动 |

|---|---|---|---|---|---|---|---|---|---|

| 稳定关联: | 非稳定关联: | ||||||||

| 通信 | 计算机 | 4 | 5 | 1 | 国防军工 | 传媒 | 66 | 598 | 532 |

| 计算机 | 电子 | 1 | 2 | 1 | 交通运输 | 机械设备 | 74 | 551 | 477 |

| 传媒 | 计算机 | 2 | 1 | 1 | 电气设备 | 建筑材料 | 143 | 587 | 444 |

| 国防军工 | 机械设备 | 12 | 10 | 2 | 国防军工 | 建筑材料 | 44 | 476 | 432 |

| 钢铁 | 采掘 | 37 | 34 | 3 | 建筑材料 | 传媒 | 109 | 525 | 416 |

| 采掘 | 有色金属 | 5 | 8 | 3 | 传媒 | 食品饮料 | 181 | 563 | 382 |

| 国防军工 | 电气设备 | 10 | 31 | 21 | 国防军工 | 轻工制造 | 574 | 203 | 371 |

| 变量 | 行业风险溢出 | 行业风险吸收 | |||||

|---|---|---|---|---|---|---|---|

| 全样本 | 危机时期 | 正常时期 | 全样本 | 危机时期 | 正常时期 | ||

| VaR | 0.0373*** (9.237) | 0.0369*** (4.440) | 0.0346*** (8.056) | 0.0577*** (22.766) | 0.0535*** (10.215) | 0.0593*** (21.774) | |

| Size | -0.0199*** (-5.220) | -0.0359*** (-4.675) | -0.0154*** (-3.715) | -0.0009 (-0.361) | 0.0047 (0.983) | -0.0009 (-0.358) | |

| Lev | 0.0655* (1.810) | -0.0642 (-0.793) | 0.0256 (0.634) | 0.0342 (1.503) | 0.1133** (2.225) | -0.0021 (-0.081) | |

| Roa | -0.1356 (-1.147) | -0.1343 (-0.547) | -0.1594 (-1.278) | 0.1044 (1.404) | 0.0994 (0.642) | 0.1009 (1.269) | |

| Growth | -0.0015 (-0.316) | 0.0016 (0.162) | -0.0015 (-0.298) | -0.0022 (-0.706) | -0.0138** (-2.236) | 0.0020 (0.625) | |

| AP | -0.0001 (-0.111) | -0.0019 (-1.156) | 0.0013 (1.564) | ||||

| AR | -0.0000 (-0.097) | -0.0000 (-0.697) | 0.0000 (0.552) | ||||

| 变量 | 行业风险溢出 | 行业风险吸收 | |||||

| 全样本 | 危机时期 | 正常时期 | 全样本 | 危机时期 | 正常时期 | ||

| Cashhold | 0.0073 (0.408) | 0.0040 (0.096) | -0.0013 (-0.069) | 0.0041 (0.367) | -0.0526** (-2.023) | 0.0221* (1.921) | |

| M2b | 0.0249 (1.214) | 0.1171** (2.321) | 0.0028 (0.139) | 0.0021 (0.160) | -0.0075 (-0.237) | 0.0131 (1.013) | |

| Gdp | -0.0004 (-0.001) | 0.0443 (1.164) | 0.0192 (0.220) | 0.3093 (0.633) | 0.0440* (1.886) | 0.0463 (0.840) | |

| M2 | 0.0023 (0.004) | -0.0808 (-1.265) | 0.0005 (0.767) | -0.2613 (-0.624) | -0.0686* (-1.742) | 0.0011*** (3.041) | |

| _cons | 0.0373*** (9.237) | 0.0369*** (4.440) | 0.0346*** (8.056) | -0.0370 (-0.637) | -0.1326 (-1.144) | 0.9248** (2.489) | |

表4 实体行业风险关联回归结果

| 变量 | 行业风险溢出 | 行业风险吸收 | |||||

|---|---|---|---|---|---|---|---|

| 全样本 | 危机时期 | 正常时期 | 全样本 | 危机时期 | 正常时期 | ||

| VaR | 0.0373*** (9.237) | 0.0369*** (4.440) | 0.0346*** (8.056) | 0.0577*** (22.766) | 0.0535*** (10.215) | 0.0593*** (21.774) | |

| Size | -0.0199*** (-5.220) | -0.0359*** (-4.675) | -0.0154*** (-3.715) | -0.0009 (-0.361) | 0.0047 (0.983) | -0.0009 (-0.358) | |

| Lev | 0.0655* (1.810) | -0.0642 (-0.793) | 0.0256 (0.634) | 0.0342 (1.503) | 0.1133** (2.225) | -0.0021 (-0.081) | |

| Roa | -0.1356 (-1.147) | -0.1343 (-0.547) | -0.1594 (-1.278) | 0.1044 (1.404) | 0.0994 (0.642) | 0.1009 (1.269) | |

| Growth | -0.0015 (-0.316) | 0.0016 (0.162) | -0.0015 (-0.298) | -0.0022 (-0.706) | -0.0138** (-2.236) | 0.0020 (0.625) | |

| AP | -0.0001 (-0.111) | -0.0019 (-1.156) | 0.0013 (1.564) | ||||

| AR | -0.0000 (-0.097) | -0.0000 (-0.697) | 0.0000 (0.552) | ||||

| 变量 | 行业风险溢出 | 行业风险吸收 | |||||

| 全样本 | 危机时期 | 正常时期 | 全样本 | 危机时期 | 正常时期 | ||

| Cashhold | 0.0073 (0.408) | 0.0040 (0.096) | -0.0013 (-0.069) | 0.0041 (0.367) | -0.0526** (-2.023) | 0.0221* (1.921) | |

| M2b | 0.0249 (1.214) | 0.1171** (2.321) | 0.0028 (0.139) | 0.0021 (0.160) | -0.0075 (-0.237) | 0.0131 (1.013) | |

| Gdp | -0.0004 (-0.001) | 0.0443 (1.164) | 0.0192 (0.220) | 0.3093 (0.633) | 0.0440* (1.886) | 0.0463 (0.840) | |

| M2 | 0.0023 (0.004) | -0.0808 (-1.265) | 0.0005 (0.767) | -0.2613 (-0.624) | -0.0686* (-1.742) | 0.0011*** (3.041) | |

| _cons | 0.0373*** (9.237) | 0.0369*** (4.440) | 0.0346*** (8.056) | -0.0370 (-0.637) | -0.1326 (-1.144) | 0.9248** (2.489) | |

| [1] |

Acharya V. V. A Theory of Systemic Risk and Design of Prudential Bank Regulation[J]. Journal of Financial Stability, 2009, 5(3):224-255.

DOI URL |

| [2] |

Diebold F. X., Yɪlmaz K. On the Network Topology of Variance Decompositions: Measuring the Connectedness of Financial Firms[J]. Journal of Econometrics, 2014, 182(1):119-134.

DOI URL |

| [3] |

Adrian T., Brunnermeier M. K. CoVaR[J]. American Economic Review, 2016, 106(7):1705-41.

DOI URL |

| [4] | 杨子晖, 陈雨恬, 谢锐楷. 我国金融机构系统性金融风险度量与跨部门风险溢出效应研究[J]. 金融研究, 2018, (10):19-37. |

| [5] |

Kiyotaki N., Moore J. Credit Cycles[J]. Journal of Political Economy, 1997, 105(2):211-248.

DOI URL |

| [6] | Bernanke B. S., Gertler M., Gilchrist S. The Financial Accelerator in a Quantitative Business Cycle Framework[J]. Handbook of Macroeconomics, 1999, (1):1341-1393. |

| [7] |

Gertler M., Kiyotaki N., Queralto A. Financial Crises, Bank Risk Exposure and Government Financial Policy[J]. Journal of Monetary Economics, 2012, 59:S17-S34.

DOI URL |

| [8] |

Brunnermeier M. K., Sannikov Y. A Macroeconomic Model with a Financial Sector[J]. American Economic Review, 2014, 104(2):379-421.

DOI URL |

| [9] | 宫小琳, 卞江. 中国宏观金融中的国民经济部门间传染机制[J]. 经济研究, 2010, (7):79-90. |

| [10] |

Chiu W. C., Peña J. I., Wang C. W. Industry Characteristics and Financial Risk Contagion[J]. Journal of Banking and Finance, 2015, 50:411-427.

DOI URL |

| [11] | Cotter J., Hallam M., Yilmaz K. Mixed-frequency Macro-financial Spillovers[Z]. Econstor Working Paper, 2017. |

| [12] |

Silva W., Kimura H., Sobreiro V. A. An Analysis of the Literature on Systemic Financial Risk: A Survey[J]. Journal of Financial Stability, 2017, 28:91-114.

DOI URL |

| [13] | 李政, 刘淇, 温博慧. 中国系统性风险度量防范研究——基于高低波动两阶段的视角[J]. 南开学报(哲学社会科学版), 2020, (5):146-158. |

| [14] | 杨子晖, 王姝黛. 行业间下行风险的非对称传染: 来自区间转换模型的新证据[J]. 世界经济, 2020, (6):28-51. |

| [15] | 李守伟, 王磊, 刘晓星, 等. 跨银行与企业部门的系统性风险研究[J]. 系统工程理论与实践, 2020, (10):2492-2504. |

| [16] | 贾妍妍, 方意, 荆中博. 中国金融体系放大了实体经济风险吗[J]. 财贸经济, 2020, (10):111-128. |

| [17] | Nguyen L. X. D., Mateut S., Chevapatrakul T. Business-linkage Volatility Spillovers between US Industries[J]. Journal of Banking and Finance, 2020, 111(2):1-26. |

| [18] | Bradley D. B., Rubach M. J. Trade Credit and Small Businesses: A Cause of Business Failures[Z]. University of Central Arkansas Working Paper, 2002. |

| [19] |

Acemoglu D., Carvalho V. M., Ozdaglar A., et al. The Network Origins of Aggregate Fluctuations[J]. Econometrica, 2012, 80(5):1977-2016.

DOI URL |

| [20] |

Alfaro L., García-Santana M., Moral-Benito E. On the Direct and Indirect Real Effects of Credit Supply Shocks[J]. Journal of Financial Economics, 2020, 139(3):895-921.

DOI URL |

| [21] |

Hautsch N., Schaumburg J., Schienle M. Financial Network Systemic Risk Contributions[J]. Review of Finance, 2015, 19(2):685-738.

DOI URL |

| [22] | 乔海曙, 李颖, 欧阳昕. 产业关联、共同信息溢出与行业股指联动[J]. 系统工程理论与实践, 2016, (11):2737-2751. |

| [23] |

Yang C. X., Zhang X. S., Jiang L. L.. et al. Study on the Contagion among American Industries[J]. Physica A: Statistical Mechanics and Its Applications, 2006, 444:601-612.

DOI URL |

| [24] |

Wu F., Zhang D., Zhang Z. Connectedness and Risk Spillover in China's Stock Market: A Sectoral Analysis[J]. Economic Systems, 2019, 43(3):1-14.

DOI URL |

| [1] | 陈张杭健, 孙磊. “双碳”目标下中国泛金融市场的动态风险溢出效应研究[J]. 财经论丛, 2023, 39(8): 47-58. |

| [2] | 赵放, 刘雅君. 人民币汇率与股市的风险溢出效应再检验——基于马尔科夫转换GARCH模型和混合时变copula模型的研究[J]. 财经论丛, 2018, 34(9): 55-65. |

| [3] | 刘建和, 王勇, 王玉斌. 沪铜期货还是伦铜期货的影子市场吗?[J]. 财经论丛, 2018, 34(4): 56-65. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||